Several years ago, I gave a private company a small loan. In exchange, I would be paid back the full amount plus 15% interest.

In addition, the company offered collateral in the form of a patent, intellectual property, and their trademark. So, if they defaulted on their loan – meaning they didn’t pay me back – I could take those assets into my possession.

I’ll tell you what happened with that loan in a little bit…

First, let’s discuss bonds very quickly.

Bonds are boring. But, there is something crazy going on in the bond market that you should know about…

Companies issue corporate bonds, cities issue municipal bonds, and governments issue sovereign bonds.

Companies issue corporate bonds, cities issue municipal bonds, and governments issue sovereign bonds.

Each of these types of bonds have a rating. The higher the rating, the more likely the bond is to be repaid. At the same time, the higher the credit rating, the lower the interest rate that is paid on the bond.

Think about it from an investor’s point of view…

Would you rather lend money to someone you know is going to pay you back, or to someone who you are not sure is going to pay you back?

Of course, all of us want our money paid back. So, how does someone who may not pay us back (or has a poor credit rating) convince someone to lend them money?

They offer very high interest rates.

The higher the credit rating, the lower the bond yield. The lower the credit rating, the higher the bond yield.

That’s why it’s very important for a company or government to have a high credit rating. That means they can borrow money inexpensively. And when you can borrow money on the cheap, you can finance projects more easily.

Now, there are all kinds of different bonds, but the key thing to remember here is risk.

The higher the risk, the higher the yield. If you are going to risk your money, then you should be paid a higher rate.

The lower the risk, the lower the yield. If you are not necessarily risking your money, then you won’t be paid extra.

Pretty simple to understand. Right?

Now… here is where it gets interesting…

In the US, the ‘average investor’ is changing their portfolio to be more reliant on bonds.

That’s because the ‘average investor’ is a baby boomer who is leaving the work force on their way to retirement. During this transition, these boomers are also rebalancing their portfolios to be heavier into bonds, because they want more reliable yield.

Remember, that’s essentially what a bond is… it’s like you are loaning money to someone and they are paying you back with interest. On the other hand, owning stocks allows for capital appreciation but not a steady flow of income.

So, these boomers are buying more bonds to transition their wealth to safer, more steady income type investments.

That has resulted in bond funds receiving $1 billion a day since January 2016.

That’s a lot of money.

In fact, there is so much demand for bonds (think steady income for investors) that bond issuers have been able to offer their debt at a much lower rate.

For example, in June, Argentina issued a 100-year bond at a yield of 8%.

But, Argentina has defaulted seven times on its international debt and five times on its domestic debt in the past century.

So, let me rephrase that for you:

Investors are lending money to a country for 100 years at a rate of 8% and this country has defaulted 7 times in the past century.

Ask yourself this question… would you loan money to someone for an 8% yield if that person has gone bankrupt 7 times?

HELL NO!!!

But, that is exactly what is happening. And it’s not just Argentina. It’s Greece, Iraq, Botswana, and many other countries who are issuing bonds right now that have histories of defaulting.

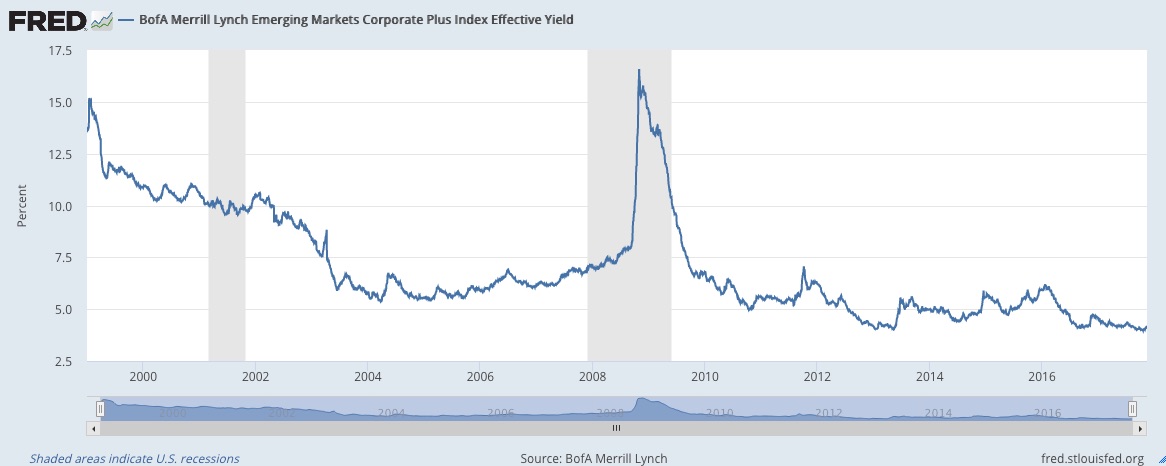

Source: FRED

Investors are so desperate for yield that they are lending their money for low returns to debtors that have histories of defaulting.

That’s crazy.

Ok, now back to the story that I originally started out with.

Remember, I loaned money to a small private company for a 15% yield. I also got some collateral just in case they defaulted.

Guess what happened to that small company?

They defaulted.

I lots all of my money, but I did get the collateral.

What’s going to happen with all of these bonds? The bonds that are being bought up at a rate of $1 billion a day?

Well, I assume that most of them will be paid back.

But, I’m also willing to bet that there will be a lot of defaults. And those bond holders don’t have any collateral, like I did with my loan.

So, when you are investing or lending money, consider what the risk is.

Consider if you should be lending money for a small return to someone who has a history of going bankrupt. Chances are they’ll do it again.